A Bicyclist's Guide to Insurance

Follow us on

social media!

Everything You Need to Know About Bicycle Insurance in 2023

If you ride a bike, chances are that you also drive a vehicle. To legally operate a motor vehicle on city and state roadways, you need auto insurance. Auto insurance is a necessity for motorists as it provides financial protection in the event of an accident. However, what many people don’t realize is that their auto insurance may also protect them in the event of a bicycle accident.

We want to believe that drivers protect themselves and carry adequate insurance, but this is not always the case. In fact, approximately 13% of all drivers on the roads are uninsured, with some states approaching nearly 30%. Additionally, the minimum policy limit requirement for automobile liability insurance coverage is relatively low, with a national average of about $25,000 per person bodily injury policy limit and in some states (like California) only requiring $15,000. To put this into perspective, over 80% of injured cyclists represented by Bike Legal incurred medical expenses in excess of $30,000.

In this guide, we will walk you through the basics of auto insurance and provide you with valuable information on how to choose the right coverages to protect yourself and your bicycle. We will dive into the different types of cycling accidents and how your auto and/or homeowners’ insurance may play a role in protecting you and your beloved bicycle. Let’s get rolling…

TABLE OF CONTENTS

- Why Cyclists Need Auto Insurance

- Crashes in 2021: A Look at Fatalities and Injuries by Category

- The Basics of Auto Insurance

- Understanding the Risks of Uninsured Motorists

- Uninsured (UM) and Underinsured (UIM) Coverage Explained

- What Are the Auto Insurance Requirements in My State?

- The Cost of Auto Insurance in the U.S.

- Common Cycling Accidents and the Types of Insurance that Cover Them

- Why Using a Camera On Your Bike Can Protect You

- Is My Bicycle Insured if it is Stolen, Damaged, or Vandalized?

- How Homeowners and Renters Insurance May Protect Your Bicycle

- Named Non-Owner Insurance Policies: For People Who Don't Own Vehicles

- What to Do if You Have Been in a Bicycle Accident

1. Why Cyclists Need Auto Insurance

As a cyclist, you might wonder why you need auto insurance when you're not driving a car. While it may seem counterintuitive, having auto insurance can be crucial for your financial protection in case of an accident involving a motor vehicle. Even if you are not at fault, medical expenses and property damages can be significant. Auto insurance may help cover these costs and provide you with peace of mind on the road.

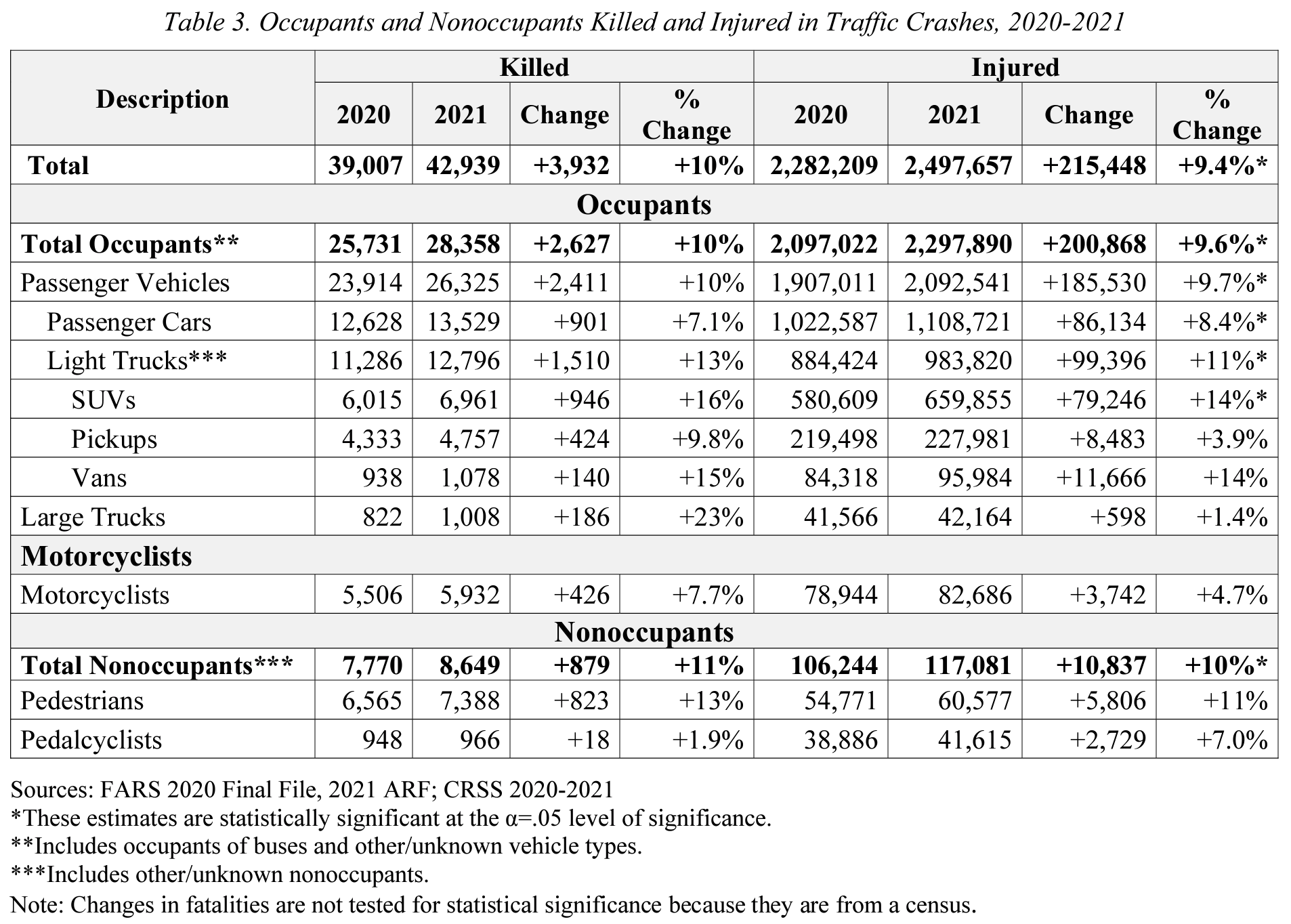

2. Crashes in 2021: A Look at Fatalities and Injuries by Category

The National Highway Traffic and Safety Administration (NHTSA) has released the latest statistics for 2021 motor vehicle traffic crashes. In 2021 an estimated 2.50 million people were injured in motor vehicle traffic crashes on U.S. roads. This is a 9.4% increase over 2020. However, we must note that due to the national shutdown in response to the Covid 19 pandemic, vehicular traffic declined in 2020.

During 2021, bicycle fatalities increased by 18, which is a 1.9% increase from 2020. 41,615 bicycle crash injuries were reported in 2021. This is an increase of 7.0% from 2020.

Florida has become the #1 state for bicycle accidents and it is also the most costly for auto insurance. Learn more about bicycle accident statistics and the top 10 States for bicycle accidents.

3. The Basics of Auto Insurance

What is Auto Insurance, and Do I Need it?

- Auto insurance is a way to protect yourself and your vehicle from potential financial burdens that can arise from accidents, theft, or other unforeseen events on the road. When you buy auto insurance, you enter into an agreement with an insurance company. You pay them a certain amount of money, called a premium, and in return, they agree to cover certain expenses caused during a motor vehicle accident. However, auto insurance won't cover maintenance or general wear and tear.

- Auto insurance covers damages to your vehicle and protects you financially if you're liable for someone else's bodily injuries and/or property damages. Auto insurance can also pay for medical bills if you are injured in an accident, or you're hit by an uninsured or underinsured driver. Your policy protects you up to certain limits, agreed upon by you and your insurer.

- Auto insurance is required in all states except New Hampshire (New Hampshire still requires financial responsibility if you cause an accident, so you'll want to be properly insured). Driving without insurance can result in a fine, license suspension, or even jail time.

Standard Types of Coverage

- Liability: To drive a vehicle legally, liability insurance is required in 49 states. If you're found at fault in an auto accident, liability coverage can pay for damage to other vehicles, damage to objects, and injuries to other drivers and their passengers. If you are being sued, your insurance carrier may provide you with a legal defense, under the provisions of your insurance policy.

-Bodily Injury Liability: Covers you if you cause an accident that injures or kills someone else. Many experts recommend carrying at least $100,00 per person and $300,00 per accident. This is often seen as 100/300.

-Property Damage Liability: Covers you when you damage someone else's property. This includes cars, fences, bicycles, and any other physical property. State laws determine the minimum amount you must purchase.

Auto liability coverage limits are typically represented by three numbers (in thousands), e.g. 25/50/25. These numbers represent how much you're covered for bodily injury per person ($25,000), bodily injury per accident ($50,000), and property damage per accident ($25,000). For personal liability coverage, you would select one total limit (e.g., $500,000), that would cover both bodily injuries and property damages in the event you caused damages to another person. These coverages are known as third-party coverages, which means they cover damages to persons other than you.

- Comprehensive: Optional Coverage that protects your vehicle caused by non-collision events outside of your control such as theft, vandalism, fire, and acts of nature. It is optional and not required by law. This coverage usually comes with a deductible and is known as a first-party coverage, which means this covers you for damages.

- Collision: Covers the vehicle if it overturns or collides with another vehicle or object, such as trees, guardrails, and fences. It is not required by law. This coverage usually comes with a deductible and is a first-party coverage.

- Medical Payments (Med Pay)/ Personal Injury Protection: Med Pay/PIP coverages can help pay for incurred medical expenses by you and your passengers if they are injured in a car accident, regardless of who is at fault. Med Pay/PIP may also apply if you were struck as a pedestrian, depending on the language of your insurance policy. However, Med Pay/PIP may not apply if you were injured while riding your bike; you will need to review the language of your insurance policy to verify coverage. It can also provide additional benefits such as reimbursement for rehab or funeral costs. It is mandatory in some states and optional in others. Med Pay/PIP are first-party coverages.

- Uninsured Motorist (UM)/Underinsured Motorist (UIM) Bodily Injury and Uninsured Motorist Property Damage (UMPD): Uninsured Motorist Bodily Injury is a first-party coverage and can provide you compensation for economic loss (i.e., medical bills, lost wages, loss of earning capacity, etc.) and pain and suffering if the accident was caused by a driver without insurance, or in a hit-and-run collision. Underinsured Motorist Bodily Injury coverage applies when the at-fault driver has insurance, but the applicable liability policy limits are insufficient to properly compensate you for your personal injuries. Unbeknownst to many people, UM/UIM Bodily Injury coverages may also apply to pedestrians and cyclists, if they were struck by an at-fault driver/vehicle. Uninsured Motorist Property Damage (UMPD) covers your property damages, usually up to a certain amount and subject to a deductible, if the at-fault driver was uninsured or underinsured. UMPD may not apply in the context of a hit-and-run collision where the identity of the vehicle or driver was not ascertained; please refer to your insurance policy to determine the applicability of this coverage. UM/UIM coverage is required in about half of the states.

- Combined Single Limit:

A provision of an insurance policy that limits coverage for all components of a claim to a single dollar amount. It offers broader coverage and has a maximum payout for any combination of injuries or property damage in an incident.

What is a Premium?

An insurance premium is the amount of money you pay to an insurance company in exchange for the coverage they provide. Think of it as the cost of having insurance. The premium is typically paid regularly, such as monthly, quarterly, or annually, depending on the terms of your insurance policy.

What is a Deductible?

The amount you pay out of pocket before insurance will cover your claim. Typically, the higher the deductible, the lower your overall premium will be. Lower deductibles carry higher premiums.

4. Understanding the Risks of Uninsured Motorists

Bicyclists and motorists alike face numerous risks on the roads, and one of the most significant concerns is the presence of uninsured motorists. Uninsured drivers are individuals who do not carry any form of auto insurance or lack sufficient coverage to pay for damages in the event of an accident. Unfortunately, the prevalence of uninsured motorists is a significant issue in many countries, making Underinsured (UM)/Uninsured Motorist (UIM) insurance crucial for both bicyclists and motorists.

Our #1 Piece of Advice for all cyclists is to carry as much Uninsured Motorist Coverage as possible.

We recommend $250k or more.

The Alarming Statistics of Uninsured Motorists

According to the Insurance Research Council,1 in 8 drivers on US roads in 2019 were driving without auto insurance. This means that approximately 13% of motorists may not have insurance coverage to compensate for injuries and damages caused in an accident. These statistics highlight the risks faced by all road users, including cyclists who share the roads with motor vehicles.

Why UM/UIM Insurance Matters

For cyclists, the risks associated with uninsured motorists are even higher. Bicycles offer less protection than cars, making riders more vulnerable to severe injuries in accidents. If an uninsured or underinsured motorist is at fault for an accident involving a cyclist, the financial burden of medical expenses, property damage, and other losses may fall entirely on the injured cyclist.

5. Uninsured (UM) and Underinsured (UIM) Coverage Explained

Uninsured motorist coverage protects you if you're hit by a driver who has no auto insurance. Underinsured motorist coverage, which is usually offered alongside uninsured motorist coverage, protects you if you're hit by a driver who doesn't have enough coverage to pay for the damages or injuries they caused. Both coverages are mandatory in many states and highly recommended for all drivers. If you're a victim of a hit-and-run accident, you can file a claim against your uninsured motorist coverage.

Uninsured and underinsured coverage is a supplemental policy that you can purchase to protect yourself against drivers who don’t have insurance or do not enough to cover your damages. Depending on your state, uninsured/underinsured motorist insurance may be separate, combined, or consist of up to four coverages:

- Uninsured and Underinsured Motorist Property Damage Coverage (UMPD):

This type of insurance coverage provides reimbursement for damage to your property caused by uninsured or underinsured drivers. This insurance coverage will provide repayment to repair or replace your vehicle and cover any other property that was damaged in an accident caused by an uninsured or underinsured at-fault driver. However, UMPD may not apply to bicycles; please refer to your insurance policy to determine the applicability of this provision.

- Uninsured Motorist Bodily Injury Coverage (UMBI):

Covers bodily injuries during an accident caused by an uninsured driver. UMBI provides compensation for medical treatment, up to the policy limit and may include Medical expenses, lost wages, Pain and suffering, and in some cases funeral expenses.

- Underinsured Motorist Bodily Injury Coverage (UIMBI):

This type of coverage is generally purchased alongside a standard UM policy. It has the same limitations in the amount that you can be compensated. To recover damages from an underinsured motorist policy, the damages you sustained must be higher than the limit on the at-fault driver’s insurance policy. This type of insurance covers bodily injuries during an accident caused by a driver who has insurance but insufficient coverage to fully compensate you for your damages. UIMBI coverage is designed to bridge the gap between the at-fault driver's liability limits and the actual costs of injuries and damages sustained in an accident.

If you have been involved in a bicycle accident it is crucial that you work with a firm such as Bike Legal that has the expertise and experience in bicycle accident claim compensation

The Difference Between UIMBI and UMBI Coverage

While both Underinsured Motorist Bodily Injury (UIMBI) and Uninsured Motorist Bodily Injury (UMBI) coverage protect in accidents involving inadequate insurance coverage, there is a fundamental difference between the two:

UMBI coverage comes into play when the at-fault driver has no insurance, while UIMBI coverage is relevant when the at-fault driver has insurance but inadequate coverage limits.

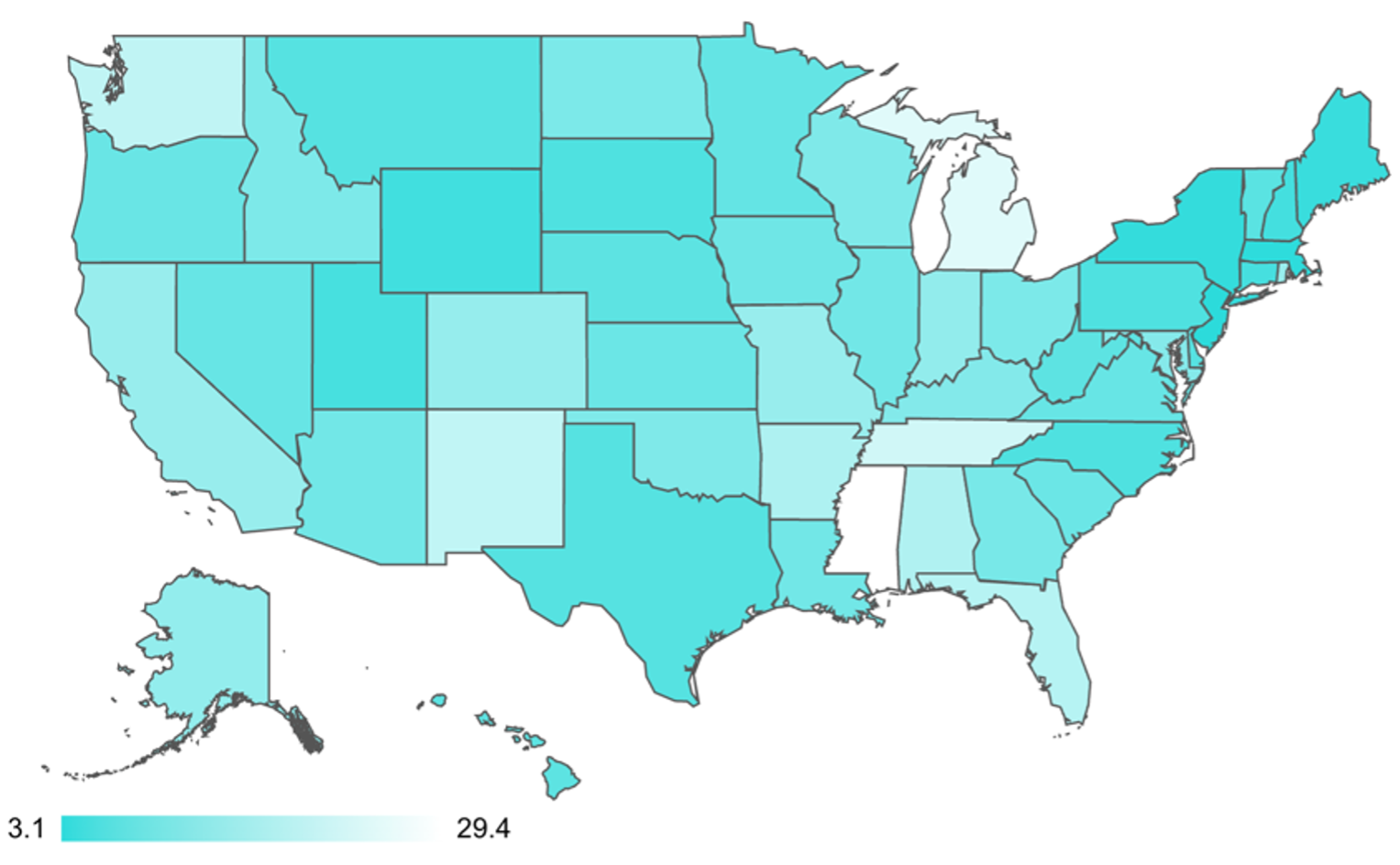

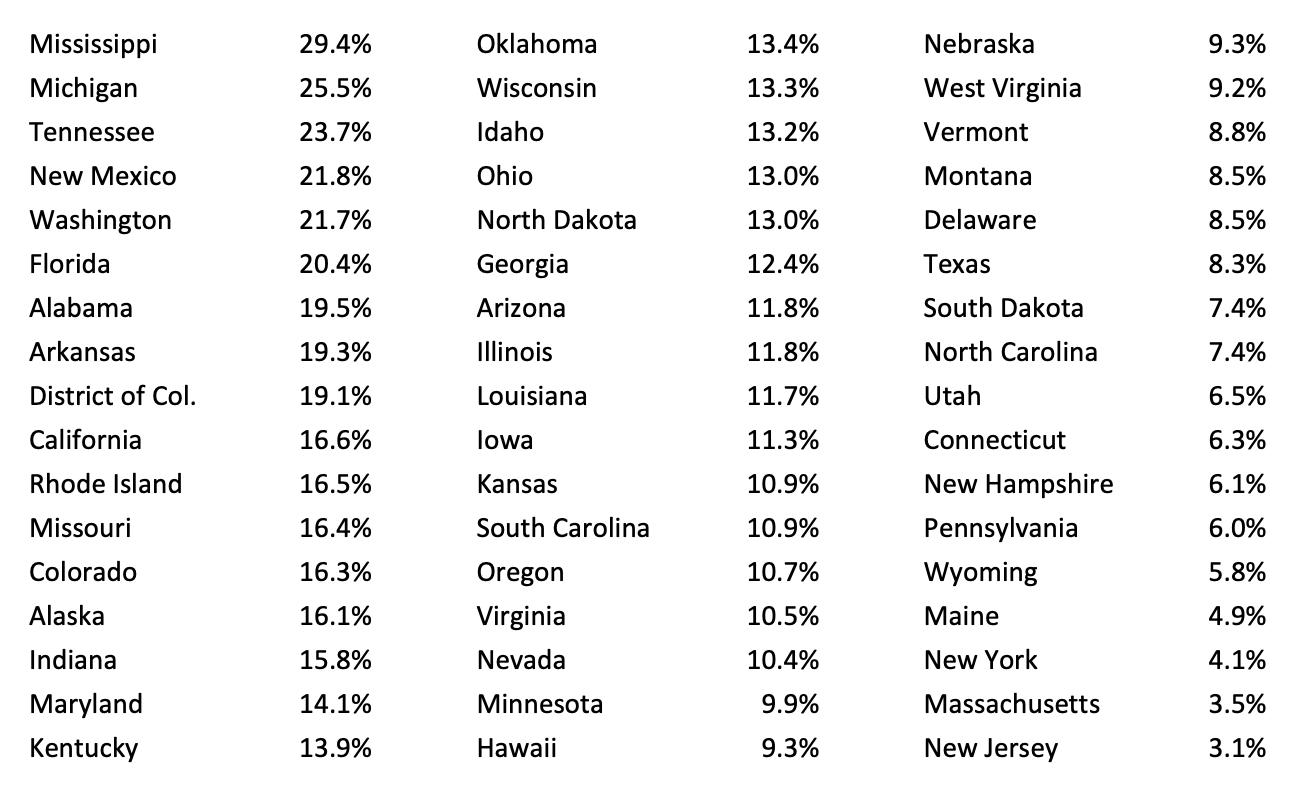

States with the Highest and Lowest Percentages of Uninsured Motorists:

During 2016, Insured drivers across the U.S. paid more than

$13 billion

for uninsured/underinsured motorist coverage.

According to a report released by the

Insurance Research Council in 2021, uninsured motorist rates varied across the U.S. ranging from 3.1% in New Jersey to 29.4% in Mississippi.

Uninsured Motorist (UM) Insurance Requirements and Costs:

Only about half the states require UM insurance. Twenty states and the District of Columbia require drivers to have uninsured motorist coverage, while 14 require Underinsured coverage.

Uninsured motorist coverage costs about $50-$70 annually for bodily injury and property damage coverage. Your actual cost will depend on how much coverage you select.

Is Uninsured Motorist (UM) Insurance Worth it?

Uninsured motorists pose a significant risk to both cyclists and motorists on the roads. With a notable percentage of drivers lacking proper insurance coverage, the need for UM insurance cannot be overstated. The more you protect yourself, the less you will have to pay out of pocket in the event of a crash. There is no reason not to purchase UM coverage aside from the small added cost to your premium.

Statute of Limitations

The statute of limitations for uninsured/underinsured motorist (UM/UIM) insurance varies from state to state. In general, the statute of limitations is the amount of time you have to file a lawsuit after an accident. If you file a lawsuit after the statute of limitations has expired, your case may be dismissed.

The statute of limitations for UM and UIM claims vary from one jurisdiction to another. You need to consult an attorney in your jurisdiction to determine the appropriate statutes of limitations for your UM and UIM claims.

6. What are the Auto Insurance Requirements for My State?

Insurance requirements vary from state to state, so it’s essential you know your requirements to be compliant. The Insurance Information Institute provides these Automobile Financial Liability Laws State by State. Other Resources that can be helpful are:

1. Contact a reputable insurance agency in your state

2. Check with your Department of Motor Vehicles

7. The Cost of Auto Insurance in the U.S.

The national average rate for full coverage car insurance is approx. $1,682 in 2023, but how much you’ll actually pay depends on where you live. Car insurance rates fluctuate significantly from state to state due to several factors. These can include your location, driving record, vehicle model, and the type of coverage you choose.

Below is a list of states with the highest and lowest premiums, key factors that influence rates, and the impact of uninsured drivers.

Car Insurance Rates by State in 2023:

A. MOST EXPENSIVE STATES:

- Florida: Ranked as the most expensive state for car insurance, with an average annual premium of $2,560, reflecting a 23% increase since 2021. This can be attributed to factors like adverse weather conditions and a high number of teen, senior, and uninsured drivers.

- Louisiana, Delaware, Michigan, and California: These states also have higher-than-average premiums due to factors such as unique insurance schemes, a high percentage of uninsured drivers, and expensive lawsuits.

B. LEAST EXPENSIVE STATES:

- Ohio: The state with the cheapest car insurance rates in 2023, with an average annual premium of $1,023, approximately 40% lower than the national average. Ohio's rates remain relatively stable compared to other states, and more individuals opt for minimum liability coverage.

- Maine, Idaho, Vermont, and Oregon: These states follow Ohio as having comparatively lower insurance rates.

Factors Influencing Car Insurance Rates:

Driving Record: A clean driving history, free from accidents or traffic violations, can lead to lower insurance premiums, as it suggests responsible driving behavior.

Location: The state you reside in influences your insurance rates. Urban areas with higher population densities, like Florida, may have increased premiums due to more traffic congestion and a greater likelihood of accidents or theft.

Coverage Options: The extent of coverage you choose affects your premiums. Comprehensive coverage, which protects against various risks such as theft and vandalism, generally results in higher premiums than basic liability coverage.

Vehicle Make and Model: Cars with higher market values or expensive repair costs tend to have higher insurance premiums, as potential claims could be more costly for the insurer.

Credit Score: In some regions, insurance providers consider your credit history when determining rates. A good credit score is typically associated with lower risk and can result in more favorable premiums.

Age: Teens and young drivers pay more for car insurance because insurance companies view them as more likely to get into accidents and file claims.

Impact of Uninsured Drivers:

Uninsured drivers raise insurance costs for everyone. Insurance companies pass on the costs associated with uninsured drivers to insured drivers. States with higher rates of uninsured drivers, like Florida, tend to have higher insurance costs overall.

8. Common Cycling Accidents and Insurance that May Cover Them

Bicycle accidents may be covered by insurance, depending on the scenario. If you're involved in a collision on your bike with another cyclist or pedestrian and you're not at fault, your medical bills and damage to your bike may be covered by the at-fault party’s personal liability coverage on their home or renters’ insurance policy. If you’re hit by a car while riding, the at-fault driver's auto liability coverage may pay for damages and injuries. If you’re at fault in a bike accident, personal liability coverage on your home or renters policy may pay for the damages and injuries you caused, up to your coverage limits.

Bicycle accidents can happen in various scenarios, and the availability of insurance coverage depends on the specific situation. In this section, we will explore common types of cycling accidents and the corresponding insurance coverage that may apply.

A. Bicycle Crashes with Motor Vehicles

- When the motorist is at fault:

If a cyclist is involved in a collision with a car and the driver is at fault, the at-fault driver's auto liability coverage may cover the cyclist's medical expenses/pain and suffering and bike repair or replacement costs. Additionally, the cyclist's health insurance may cover the cost of treatment. If the at-fault motorist is uninsured, coverage for bike damages depends on how the bicycle is insured under the cyclist's home or renter's policy. In some cases, the cyclist can pursue legal action against the uninsured driver for damages and injuries.

- When the cyclist is at fault:

If the cyclist was involved in a crash where they were at fault, their personal liability coverage under their homeowners or renters’ insurance policy may cover the other party’s property damage and injuries. The cyclist's medical expenses may be covered by their health insurance, and bike damages may be covered if they have specific coverage for the bicycle on their homeowners or renters insurance policy.

B. Hit and Run By Motor Vehicle:

If a cyclist is involved in a hit-and-run incident where the driver cannot be located, their health insurance may cover the cost of medical treatment. This is where it is imperative to have Uninsured Motorist coverage added to your policy PRIOR to being involved in an accident, as this UM insurance can also cover costs associated with hit-and-run incidents.

C. When Two Cyclists Collide (no motor vehicle involved)

- When you are at fault:

If you are on your bicycle and cause an accident with another cyclist, your liability coverage from your homeowners or renters insurance may cover the costs of the other cyclist's injuries and property damages. Costs for your injuries may be covered by your health insurance. The cost to repair or replace your bike may be covered by your homeowners or renter's insurance. Check with your insurance carrier to see if you need a specific insurance rider to cover your bicycle.

- When the other cyclist is at fault:

If another cyclist causes you to crash (this may not include bicycle races or cycling events where you have signed a release of liability waiver), your injuries and property damages may be covered under their personal liability coverage on their homeowners or renters’ insurance.

D. Bicycle Crashes due to Unsafe Road Conditions or Other Stationary Objects:

Your health insurance may cover your injuries, and your homeowners or renters insurance may cover damages to your bicycle. If the crash was due to negligence by others (such as unmarked road construction) you may be compensated for your injuries and damages by working with a bicycle accident attorney such as Bike Legal.

E. Bicycle and Pedestrian Collision:

- You are at fault for a collision with a pedestrian:

The cyclist's homeowners' or renters’ liability insurance may cover the pedestrian's injuries and any property damages. The cyclist's injuries may be covered by their health insurance. Property damages to the bicycle may be covered under their homeowners or renter’s insurance.

- The pedestrian is at fault for your crash:

If the pedestrian wanders in front of you causing you to crash, your injuries and property damage may be covered by their liability insurance under their homeowners or renters policy

F. Bicycle Crashes Caused by Dogs or Other Unrestrained Domesticated Animals:

In cases where a crash is caused by a dog or other animal, the applicable insurance coverage may vary. It is important to consult with a law firm such as Bike Legal which has expertise in these types of cases.

9. Why Using a Camera on Your Bike Can Protect You

Many cyclists attach a GoPro or other small video camera to the front of their bike or helmet. There are also taillight/camera combinations that are fantastic for capturing video and alerting of dangers from behind. The video footage makes it easier to determine fault and might be used as evidence if you're involved in a bicycle accident. The Garmin Varia pictured above has a light, camera, and radar that alert the rider of vehicles approaching from behind.

10. Is My Bicycle Insured if it is Stolen, Damaged, or Vandalized?

Your homeowner or renters’ insurance may cover your bicycle, but it's important to be aware of any special limits. Some policies have a maximum coverage limit for bicycles, such as $2,000. If your bike is worth more than that, you may need to add additional coverage. Contact your insurance carrier to determine if you require a separate rider for your bicycle(s) or if your policy covers the full value. Additionally, consider your deductible and compare it to the cost of repairing or replacing your bicycle.

According to the FBI 2019 Crime Statistics in the US, 154,009 bicycles were reported to the police as stolen. In reality, this number is most likely doubled if you include all the unreported bicycle thefts. That means a bicycle is stolen about every minute in the United States. The cities with the highest bike crime are New York and San Francisco.

To ensure you are covered:

- If your bike is stolen, damaged, or vandalized, your homeowners or renter’s policy may cover the current value of your bike, up to your coverage limit and after deducting the applicable deductible. Discuss your policy with your insurance provider to make sure it meets your needs.

- Remember to promptly report the theft to the police and provide all necessary documentation to your insurance company when making a claim.

- Read these tips on what to do if your bicycle gets stolen.

11. How Homeowners and Renters Insurance Can Protect Your Bicycle

Currently, there are no state laws mandating homeowners insurance, but, if you finance your home, your lender will typically require a home insurance policy. The standard coverages for homeowners insurance are generally the same in all states. Oftentimes, landlords and property owners will require renters’ insurance.

12. Named Non-Owner Insurance Policies: For People Who Don't Own Vehicles

A lot of people don’t own vehicles and therefore don’t have auto insurance. If you're a cyclist who doesn't own a car, there's still a smart insurance option that may be tailored just for you:

Named Non-Owner Insurance policies. These policies provide coverage even if you don't have your own vehicle or auto insurance. So, when you're pedaling away on your bike, you may not be left without protection. Named Non-Owner Insurance steps in to cover you in case of accidents or mishaps involving vehicles, whether you're riding your bike, renting a car, borrowing a car, or using a ride-sharing service.

Named Non-Owner Insurance policies vary by state and by providers.

The greatest benefit for cyclists

is the ability to add

Uninsured/Underinsured supplemental coverage.

Common Benefits of Non-Owner Insurance Policies:

- Provides liability coverage

- May provide medical payments

- Option to add Uninsured/Underinsured Motorist Coverage

- Provides rental car coverage

- May provide coverage when you borrow a vehicle

- Your insurance history is like a credit history. There’s a benefit to building your insurance history even if you don’t drive a vehicle.

- Low cost for so many benefits

There are several limitations to Named Non-Owner Insurance policies, and these vary by state, insurance provider, and of course, the coverage you select. Contact a reputable insurance provider in your state to discuss the options available to you.

13. What to Do if You Have Been Involved in a Bicycle Accident/Crash:

Being involved in a bicycle accident can be a stressful and overwhelming experience. Here are the important steps to take if you find yourself in this situation:

1. Ensure Safety: First and foremost, prioritize your safety and the safety of others involved. Move to a safe location away from traffic if possible. If you or anyone else requires immediate medical attention, call emergency services right away.

2. Gather Information: Collect information from all parties involved in the accident. This includes their names, contact information, insurance details, and license plate numbers. If there are witnesses present, try to obtain their contact information as well.

3. Document the Scene: Take photos or videos of the accident scene, including any damage to your bicycle, other vehicles involved, and any visible injuries. These visual records can be valuable when filing an insurance claim or seeking legal recourse.

4. Contact the Authorities: Depending on the severity of the accident, it may be necessary to report it to the police. They can create an official report detailing the incident, which can be useful for insurance purposes and legal proceedings.

5. Seek Medical Attention: Even if you feel fine immediately after the accident, getting a medical evaluation is crucial. Some injuries may not be apparent right away, and a healthcare professional can assess your condition and provide necessary treatment. Keep copies of all medical records and bills related to the accident.

6. Call Bike Legal at 877-Bike Legal. Contacting a bicycle accident attorney can help protect your rights, navigate legal complexities, and pursue appropriate compensation. Consultations are free.

7. Don't Negotiate on Your Own: Don't let insurance companies take advantage of you. Navigating insurance companies and opposing parties can be an overwhelming task. However, by engaging the services of a bicycle accident lawyer at an early stage, you can alleviate the burden of communication and negotiation. Their primary focus will be advocating for your best interests, diligently working towards securing equitable compensation for medical expenses, lost wages, pain and suffering, and any other damage arising from the accident.

8. Keep Records: Maintain a file of all relevant documents related to the accident, including police reports, medical records, correspondence with insurance companies, and any expenses incurred. These records will be valuable in supporting your case and ensuring a fair resolution.

Remember, each bicycle accident is unique, and the appropriate actions may vary depending on the specific circumstances. It's always recommended to consult with legal professionals who can provide personalized guidance based on your situation.

Are You Adequately Covered?

As a cyclist, being informed about the various types of insurance is crucial for your safety and financial well-being. Understanding liability coverage, uninsured/underinsured motorist coverage, personal injury protection, and comprehensive coverage will help you make informed decisions when selecting insurance coverage. Remember to adhere to legal requirements to avoid potential penalties. By taking the time to learn about auto insurance, you'll be better equipped to protect yourself and your bicycle in the event of an accident. Stay safe on the road and enjoy your cycling adventures with the confidence of adequate insurance coverage.

At Bike Legal our mission is to

advocate for bicycle safety and sharing the road responsibly through education.

Our legal team is committed to supporting and representing cyclists

across the United States no matter where you ride or how you ride.

If you or someone you know has been involved in a bicycle accident,

Bike Legal is here to help!

Visit: www.bikelegalfirm.com

or call 877-BIKE LEGAL (877-245-3534)

Bike Legal Spoke & Law Blog

If a Driver Seriously Injures or Kills Someone, Are They Automatically Tested for Drugs and Alcohol?

California’s Landmark Electric Bicycle Safety Study Reveals Why Regulating E-Bikes Is So Complicated

Ride Protected

Ride Safe, with Bike Legal

At Bike Legal, our mission is to advocate for bicycle safety and to share the road responsibly through education. Our legal team is committed to supporting and representing cyclists across the United States, no matter where you ride or how you ride.